The Debt Threshold

Balancing leverage with returns

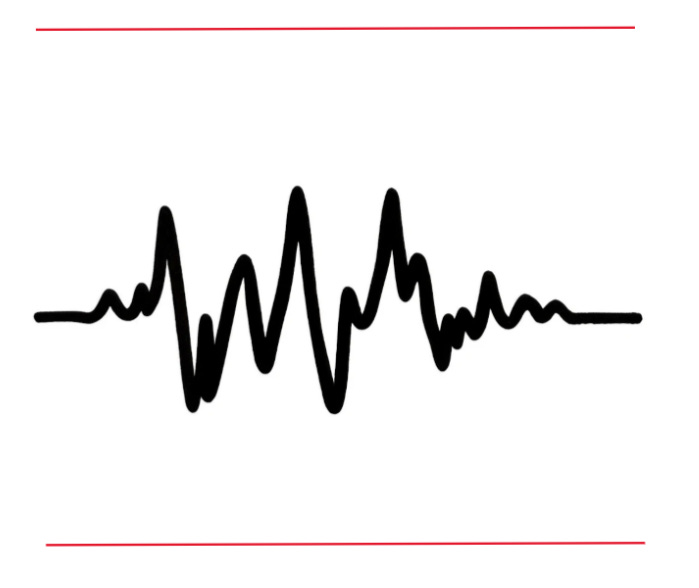

Picture from Meiji University

Morgan Housel wrote an insightful piece on debt [accessible here] where he discusses Japan's unique landscape of enduring companies, some of which have been around for at least 500 years, having endured wars and other calamities. He goes on to say that their sustained success has to do with their minimal reliance on debt which improved their long term positions.

I couldn’t agree more and we have seen other enduring companies follow a similar path. At the end, he concludes by saying “There’s a time and place, and used responsibly it’s a wonderful tool.’

So what is this time and place for debt? And how do you determine whether debt is right for your company?

There is no fixed answer to this question; instead one should be aware of their own cyclical nature and ‘breaking-point’. Failing to understand your company’s true cyclical nature will prevent you from being equipped to take on any amount of debt.

For example, in Housel’s article he includes the following picture to explain how a company endures with no debt:

The logic here is that without debt, a company can withstand extreme outlier events (let’s refer to them as black swan events), such as wars, calamities, pandemics, leadership shake-ups, and so forth.

The question is, are all companies created equal in terms of volatility? Definitely not, and I don’t think Housel was trying to state that in the article. He simply explained that having minimal debt allows any company to be more nimble under all circumstances and gives them a sustainable long term advantage. The drawing was meant to illustrate that.

There may be situations where the most extreme outcomes remain within a margin of safety from the breaking-point under a no-debt scenario. In such cases, it can look more like this:

Here we encounter fundamentally strong companies capable of withstanding economic shocks better than others. These firms are less cyclical, with lower risk and more consistent returns. In such cases, debt can work wonders, serving as a lever to magnify returns. Think of companies with uncorrelated and diversified assets, such as Amazon1, Berkshire Hathaway or Koch Industries.

As a company strengthens and its assets become more diversified and uncorrelated, it gives them more power to use leverage.

You end up with a situation like the following:

These types of companies can utilize debt to enhance returns, without being vulnerable to black swans events.

People have an innate preference toward immediate gratification—it's human nature to prioritize the present over the future ('bird in the hand'). For many, the allure of instant wealth often outweighs the benefits of long-term returns, even if long term returns can generate significantly more wealth. Most people would rather have a BMW and a nice house with high debt over a small apartment and a Civic with no debt. And from a business standpoint, most would favor rapid growth in the short term2 (driven by optimistic views), rather than making sacrifices now for a more robust long-term outcome.

Understanding the true long term costs while minimizing the temptation for short term gain will benefit anyone in business and in life. The most successful individuals and businesses understand this tendency well and avoid it at all cost. It’s their secret weapon. The truth is, only a handful of entrepreneurs and investors understand this, or maybe most do but their innate human tendencies are so strong that it prevents them from doing so. This is why we see huge swings in the market (boom and bust).

Going back to debt and to the Japan example, we see a purist form of this creature in Berkshire Hathaway. In Buffett’s last shareholder letter, he states something interesting:

Occasionally, markets and/or the economy will cause stocks and bonds of some large and fundamentally good businesses to be strikingly mispriced. Indeed, markets can – and will – unpredictably seize up or even vanish as they did for four months in 1914 and for a few days in 2001. If you believe that American investors are now more stable than in the past, think back to September 2008. Speed of communication and the wonders of technology facilitate instant worldwide paralysis, and we have come a long way since smoke signals. Such instant panics won’t happen often – but they will happen.

One fact of financial life should never be forgotten. Wall Street – to use the term in its figurative sense – would like its customers to make money, but what truly causes its denizens’ juices to flow is feverish activity. At such times, whatever foolishness can be marketed will be vigorously marketed – not by everyone but always by someone.

Your company also holds a cash and U.S. Treasury bill position far in excess of what conventional wisdom deems necessary. During the 2008 panic, Berkshire generated cash from operations and did not rely in any manner on commercial paper, bank lines or debt markets. We did not predict the time of an economic paralysis but we were always prepared for one.

Extreme fiscal conservatism is a corporate pledge we make to those who have joined us in ownership of Berkshire. In most years – indeed in most decades – our caution will likely prove to be unneeded behavior – akin to an insurance policy on a fortress-like building thought to be fireproof. But Berkshire does not want to inflict permanent financial damage – quotational shrinkage for extended periods can’t be avoided – on Bertie or any of the individuals who have trusted us with their savings.

Berkshire is built to last.

Berkshire Hathaway bears resemblance to the Japanese trading houses, which is why it's unsurprising that Berkshire owns roughly 10% of the big 5. They share similarities with the 'Shinise' mentioned in the article, but with a big caveat: Berkshire generates a substantially higher return-on-capital while maintaining the same dedication to cash and debt-avoidance.

That said, Charlie Munger believed that Berkshire would be worth double if they used some debt, with minimal downside.

“Berkshire could easily be worth twice what it is now. And the extra risk you would’ve taken would’ve been practically nothing. All we had to do is just use a little more leverage that was easily available”

Charlie Munger

What Munger is trying to say is that the returns volatility of any of Berkshire’s companies is so distant from the critical zone, and their return-on-equity is so attractive, that incorporating some debt could have greatly benefited them. It would have appeared like this:

Why didn’t they do this? Some individuals cannot withstand even a few quarters of negative returns. It’s important to understand that when leverage is used, losses magnify. Any negative black swan events would have created more volatility in the stock, which not all shareholders are used to.

Don’t get me wrong, I do prefer to be less reliant on debt and would prefer to stick to businesses that don’t need it, but there are times when your return-on-equity far exceeds (within a margin of safety) the cost of debt that it makes sense to apply the right kind of leverage to boost returns.

Failing to do so may cost you a fortune in the form of opportunity cost that you will only realize when it is too late.

ABOUT THE AUTHOR

Keenan Ugarte is Managing Partner at DayOne Capital Ventures, an independent private holding company based in the Philippines that partners with entrepreneurs across a wide range of industries. He is the Co-Founder and Director of The Independent Investor.

I know their ecommerce solutions could be irrelevant 20 years from now (we just don’t know), but they have built more than just an ecommerce site and continue to reinvest dividends into other businesses that are unrelated to each other. See article here to learn about how they manage debt.

Another aspect of this is the preference for dividends over retained earnings. The whole idea of not paying dividends goes against the fabric of what is taught in business schools despite it having huge benefits for growing companies due to compounding.