The Google Deal

A compounding bet with an AI call option

I’ve spoken to a few people about Berkshire’s $10 billion Alphabet investment, and many seem to label it as a statement of pure AI conviction.

I think the deal structure shows something very different.

At a 6.3% discount (priced at $351.81/share), Berkshire is not getting a classic Buffett rescue package. No preferred coupon. No warrants. No obvious downside protection. It is buying pure common equity. So what’s the catch of all this? Why would Berkshire, who is so accustomed to having a higher returns threshold, spend time and money on Alphabet?

On my back of the envelope math, that means Berkshire is effectively starting with something like a 2.5%–3.0% normalized owner-earnings yield on Google’s core sticky business.

What are those businesses?

Google Search

YouTube

Android

Chrome

Google Maps

Gmail

Google Workspace

Google Play

Google Cloud Platform

Google One / consumer subscriptions

Google Photos

Google Drive

Google Ads / ad network

Pixel and devices ecosystem

That yield could even be higher if we assume actual maintenance capex is lower than stated depreciation, but those are conservative numbers: 2.5%–3.0%

The sticky revenue base is still strong. These are not speculative businesses. They are deeply embedded in our daily lives and the odds of them going away, rain or shine, are quite low.

So the question is not really: “Is Berkshire betting on AI?”

The better question is:

Why would Berkshire accept such a low starting owner-earnings yield?

Historically, Berkshire has not been one to overpay for speculative growth. So why do this now, near what many would call an inflated market?

The only way I can make sense of it is as a kind of call option.

Not a literal option. Berkshire did not receive warrants or kickers that he usually adds in rescue packages (i.e. Goldman and Occidental deal). But instead they used common equity in Alphabet, which gives them option-like exposure to AI if the current compute buildout turns into a large future profit pool.

The base case is that Berkshire buys Google’s sticky core revenues at a 2.5%–3.0% normalized owner-earnings yield. Then those owner earnings compound.

In Q1 2026, Google Services made $40.6 billion in profit. In Q1 2023, Google Services made $21.7 billion in profit. In Q1 2026, Google Cloud’s profit was $20 billion, In Q1 of 2023, it was $0.2 billion. That’s a compounded annual return (CAGR) of ~23% for Google Services and 220% for Cloud.

Another thing: over the last 10 years, Googles core operating profits hit a CAGR of 22.3%.

But Uncle Warren doesn’t speculate. He wants to know downside.

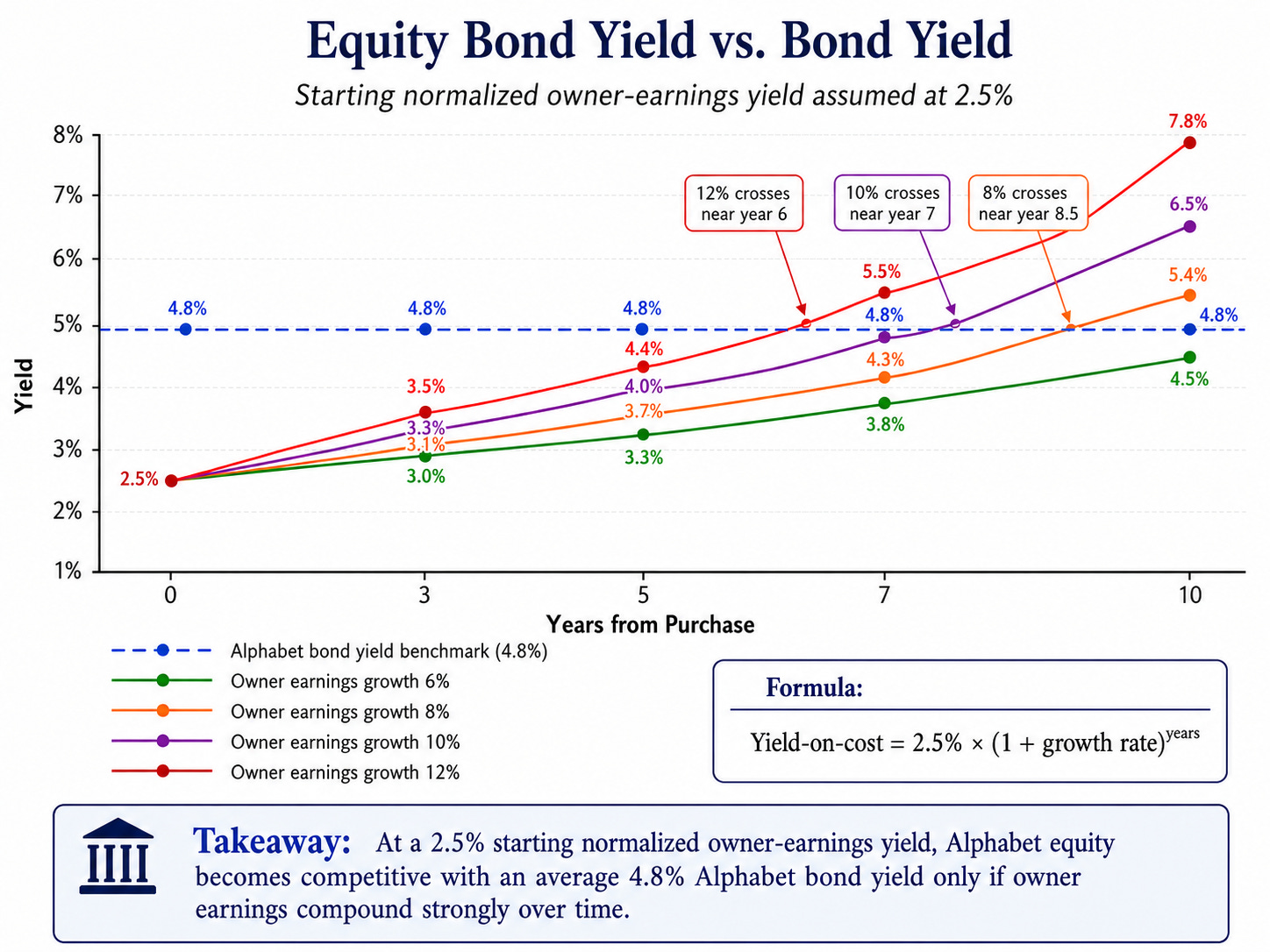

Let’s assume owner earnings grow at 6%, 8%, 10%, or 12% annually.

Starting at a 2.5% normalized yield, the yield-on-cost after ten years becomes roughly:

6% growth: 4.5%

8% growth: 5.4%

10% growth: 6.5%

12% growth: 7.8%

Her is a graph that shows the owner earnings yield relative to Google’s benchmark bond rates:

That is the whole bet.

At the start, Alphabet equity yields less than Alphabet bonds. But if owner earnings compound at a high single digit rate or better, the equity yield-on-cost eventually overtakes the bond yield. And unlike bonds, equity has no capped upside.

So this is not a “cheap stock” in the traditional Berkshire sense, nor is it considered “fair in price”. They are uncertain on where AI will go, and given the growth and durability they are seeing in the short run, they are willing to live with an acceptable “bond like” downside yield with a triple A company like Alphabet, so long as they have a chance to participate in upside (if any).

It is more like:

Heads, Berkshire owns a compounding Google franchise with enormous AI upside. Tails, it still owns one of the best sticky revenue businesses in the world, and may get a chance to buy more at a better price in the next crisis.

I am using the Mohnish Pabrai framework of “Heads I win, tails I don’t lose much.”

That second part matters. If AI disappoints, Berkshire is not finished. If the core Google business remains durable and the stock reprices lower, Berkshire can double down at a higher owner-earnings yield. Even at worst case scenario, he will be able to capture upside by buying low if that ever happens. The Google Suite is not going away.

That is very Berkshire.

Start with a wonderful business. Accept a modest initial yield. Let time and compounding do the work. And keep enough capital available to be aggressive if the market gives you a better price later.

Best case? Alphabet’s AI compute buildout becomes a massive new profit pool.

Base case? Google’s sticky core keeps compounding.

Worst case? The market punishes the stock, but Berkshire still owns a durable cash machine and may get to buy more cheaper.

That to me is the real deal.

A compounding bet on $10 billion, with an AI call option attached.

ABOUT THE AUTHOR

Keenan Ugarte is Managing Partner at DayOne Capital Ventures, an independent private holding company that invests in and builds high-growth, early-stage businesses that serve the Philippine mass market.

I like your analysis of Berkshire decision. It is an opportunist investment with a plan for Abel