In July 2025, I placed a bet on a brand that kept me up at night. It was my first concentrated position outside of Berkshire Hathaway Class B. I hesitated for weeks before finally pulling the trigger.

Hershey’s was being punished by three negative catalysts hitting at the same time:

(1) the rise of Ozempic and its perceived impact on consumer preferences,

(2) tariff-related cost pressures, and

(3) a sharp spike in cocoa prices, with global warming front and center.

A perfect storm.

I spoke with other investors and “smart” forecasters, many of whom trade commodities for a living, stare at charts all day, and understand cocoa deeply. The consensus was clear: cocoa prices were here to stay, and people were eating less chocolate.

As a result, Hershey’s stock price tanked since May 2023. The outlook was all pessimism.

I asked myself a few simple questions back in July:

Will people really stop spending on chocolate?

Will parents stop buying Hershey’s for holidays and Christmas parties?

With roughly three-quarters of Hershey’s portfolio priced at $4 or less, would modest price increases meaningfully destroy demand? Would I stop buying a chocolate bar if it cost 20 cents more?

Fundamentally, is the business actually deteriorating?

Will Ozempic really wipe out a brand that has endured for over 100 years and was built across generations?

Every time I traveled, I asked duty-free cashiers which chocolates sold the most. The answer was always the same: Hershey’s. I asked specialty chocolate store clerks whether volumes had fallen. They had not. This was consistent across countries, airports, and stores during my summer trip last year (in the US, Southeast Asia, and Europe).

Fundamentally, the numbers told the same story.

One framework that helped me think clearly through this pessimism comes from Joel Greenblatt and Warren Buffett. It is the Equity Bond approach. The idea is simple. Treat owner earnings like a bond coupon. Instead of dividing a coupon by the bond price, divide owner earnings (I like adjusted and normalized EBIT as a measure) by market capitalization. The result is an equity yield, which shows how much earning power (and eventually cash) the business produces for owners at today’s price. Buffett has often said that stocks can be viewed as bonds with variable coupons.

This framework is especially useful during periods of excessive pessimism. When excessive pessimism occurs, prices (market capitalizations) collapse, but not necessarily the owner earnings.

And there is a law in value investing that stands the test of time: price eventually catches up to yield.

Long story short, Hershey’s was trading at such an attractive yield, which I posted about here.

Another thing with equity bond yield. You can compare them to the 10 year treasury to show the return differential relative to risk. At this time it was widening.

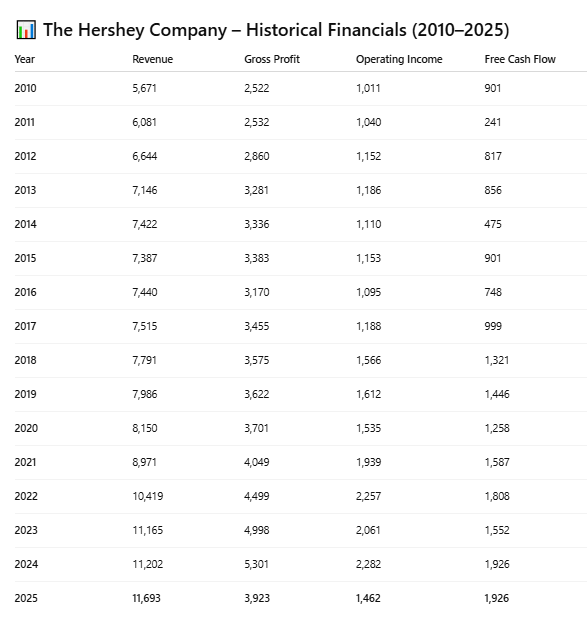

This is a company with:

A brand built over decades

Free cash flow growth averaging ~5-10%% annually

Consistent FCF margins of 12–18% since 2010

~$1B in cash on hand as of end of 2025

And check this out:

This long term performance is impressive.

Yes, 2025 was painful, but is it enough to destroy the long term potential of its brand and product? And did the price justify it?

At the time of my investment, Hershey’s equity bond yield was above 10 percent, assuming a conservative case with cocoa prices remaining elevated. In my mind, there were two paths:

Outcome A: Cocoa prices stay high, and I earn roughly 10 percent annually over the long run from a dominant brand. Price follows yield.

Outcome B: Cocoa prices fall, and Hershey’s earnings rebound sharply with potential for anything above 10%. Anything above 10% would be generous for a brand like Hershey’s. Again, thinking of it like a bond.

I viewed both outcomes as roughly equally probable. I did not bother modeling Plan B further. The upside would take care of itself. As Joel Greenblatt says, “Look down, not up.”

And then something started to happen…

Cocoa prices started dropping from its all time highs by end-of-July.

and then by November, Trump cancelled tariff’s on key agricultural products in the US, including cocoa.

And people were still buying chocolate bars…

At this time it was clear that outcome B had played out and the upside scenario was at play. You can be sure that Hershey’s turned a headwind into a tailwind, and time will tell how much further this stock will go,

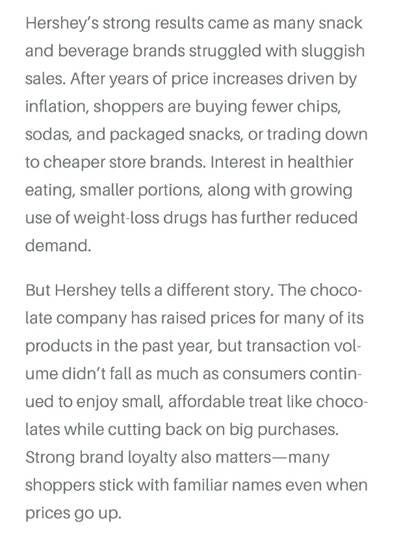

That said there is an important lesson here. Hershey’s has a powerful brand. So powerful that even with these headwinds, they have the ability to increase prices. When a company has a brand as strong as Hershey’s (just like Coca Cola), gradual price increases don’t affect demand. People trust it. This was forgotten when the macro headwinds collided. As earnings came out and as the price adjusted upward, a Barron’s article came out with a good point worth mentioning

https://www.barrons.com/articles/hershey-stock-earnings-41f7db9e

“Many shoppers stick with familiar names even when prices go up”

Outcome A would have resulted in gradual price increases over time for each chocolate bar, and a decent yield on Hersheys. Outcome B would have been all upside. It was a good bet.

This was always a long-term holding for me and I won’t be selling for the foreseeable future, at least five years and potentially forever. Hershey’s is a classic compounder, as its long-term history shows. The challenge with great compounders is usually valuation (they tend to be expensive). That was not the case here. When multiple negative narratives collide, excessive pessimism creates opportunity for those willing to focus on fundamentals and price.

Six months is far too short a time frame to judge success. There will be volatility along the way.

But history rhymes. A company with a century-old brand, pricing power, consistent free cash flow margins of 12 to 18 percent since 2010, and roughly $1 billion in cash at the end of 2025 does not strike me as a business facing existential risk.