Disclaimer: This is just my personal opinion and not investment advice. I may be wrong. Please do your own research before making any investment decisions.

How I stumbled upon it.

Generally, the way I like looking for companies is through catalysts. Things that make a stock move up or down that are more macro in nature, or driven by emotion. Think politics, wars, recessions, tech booms, failed investments, lawsuits, you name it. Things that might temporarily change perception outside of fundamentals. There are many types of catalysts and each one affects a company differently. They all affect the “madness of crowds”, which can push stock prices away from their true fundamentals.

I used to use Joel Greenblatt’s screener, but since AI has become more advanced, I’ve switched to Gemini and ChatGPT to screen companies based on Return on Invested Capital (ROIC). The ultimate high level screener for good companies.

Simply put, high ROIC businesses generate returns on invested capital way in excess of their cost of capital, which means they tend to be strong companies with a moat. Especially if ROIC is consistent (which you can historically track over the years). Companies with strong ROIC tend to be expensive as reflected in the typical ratios (P/S, P/E, etc.). This does not make them an automatic “buy” candidate. In fact, only a rare few deserve an investment. There is always a price to great returns.

Long story short, I bumped into a company as I was looking for new inventions on the internet (I was bored). A name popped up about a company that uses historical patent information, academic papers, and others, and provides insights to decision makers who are working for some of the largest R&D divisions in the world. This was Clarivate (CLVT). It was listed as one of the world’s leader in this space. Think of Google, Microsoft, Stanford, Bloomberg, the US government, and some of the biggest insitutions. Every year they have a budget for R&D and if they invent new things, they have to make sure that thing does not infringe on any existing patents or trademarks. So what does the head of R&D do? He calls their lawyer, who then uses CLVT to check whether new inventions don’t violate any existing patents. Or, the company can just have an analyst internally who can do the job. Not only that, it can also show him what makes those patents and trademarks different. This information is then used to modify the product further to ensure that the insitution is not infringing upon existing patents.

As a quick check, this was a company that was easy to understand. Enough for me to know that it is a need and one that could potentially be sticky (as validated with some users that I know).

Companies with big R&D budgets use CLVT’s tools, often through their IP teams or legal counsel, to assess prior art, avoid patent infringement, and guide innovation strategy. And since CLVT has exclusive information on certain patents and trademarks, it has an edge over just data analytics and AI. CLVT does not suggest or redo their inventions, but provides the data and insights that help experts make informed decisions about how to proceed using their exclusive information. This is critical for all the biggest companies and insitutions.

For example, Nissan just signed up with one of their tools in December:

You might say “well can’t AI already do this?”. The difference here is that CLVT has exclusive data over many years going back decades that allows them to build upon their insights. Which keeps their moat intact. Think of how Bloomberg is for the finance world, but in this case it isn’t live information. Sure AI can organize data in any way it wants, but you need the data in the first place. Some manually submitted and others sought out. Companies need this data to ensure that they are ahead of the curve as it relates to innovation and whether internal innovations don’t violate existing frameworks.

Some other facts (from their annual report):

Nearly all the world’s top 400 universities use Clarivate solutions to accelerate research and enhance education.

All the world’s top pharma, medtech, and biotech companies rely on Clarivate to improve patient outcomes.

More than 95% of the world’s top 50 R&D companies work with Clarivate to accelerate innovation.

When I look at companies, I like to see how investors have been rewarded over time. And when I read about CLVT, I automatically assumed investors would have been rewarded given their high ROIC (adjusted) and cash flows.

If they haven’t been, then there is usually a story behind it. Something else affecting the company that might be worth digging into.

If a company provides a service that is critical for patents (especially in this new age of AI, Robotics, life science etc.), with a moat and high ROIC, investors should be rewarded over time.

This is not the case with CLVT.

Since the end of 2021, shareholders have lost roughly 92% of their wealth.

Ouch.

This made me ask a simple “why?”. How can a company that provides such a critical service to institutions lose so much shareholder value?

This made me dig a little deeper.

Brief History of Clarivate

Clarivate is a 9 year old company, having spun off from the Intellectual Property & Science business of Thomson Reuters back in 2016 as a private company. So the service has been around for a much longer time. There are many reasons why a company would spin-off from another company, and in this case, the intellectual property & science division (IP&S) of Thomson Reuters was not core to their operations, so they figured they could spin it off and raise the necessary capital to focus on their other divisions: legal and regulatory information, news, and tax/accounting. Their bread and butter.

So who bought this spun-off company back in 2016?

Enter private equity.

In July 2016, Thomson Reuters agreed to sell their entire IP&S to Baring Private Equity Asia (BPEA) and Onex Corporation for about $3.5 billion in cash.

Side note:

When private equity firms invest in companies, they tend to like: (1) high cash flow businesses (to support leverage), (2) businesses with stable and growing operating income, (3) companies with strong moats. They have a heavy hand at the board level and usually aim for a liquidity event 5-7 years later. So their incentive is buy, optimize, and sell at a much higher value… now back to the story.

Onex and Baring Asia together made an equity investment of about $1.6 billion for 100% ownership.

At closing, the business transitioned from being a division inside Thomson Reuters into a standalone company owned by the private equity owners and managed under its own leadership.

What happened next?

From 2016 to 2019, CLVT operated as a private, PE owned company. It was a cash-flowing, leveraged information services platform. It had clear gross profits, stable operating earnings and cash flows. They did not do much in terms of driving growth but instead to streamline.

By 2019, SPACs were gaining momentum and became an attractive route for private equity owned companies to go public.

Side note:

SPACs are already listed shell companies that merge with private businesses, allowing private businesses to access public markets more quickly than a traditional IPO. There are other nuts and bolts around how this is done but this is the gist of it.

CLVT listed through a SPAC by mid 2019 (through a compay called Churchhill Capital Corp. III). Remember, while some SPAC transactions raise growth capital, in CLVT’s case the transaction primarily served as a pathway to exit for the private equity owners.

Soon after this event happens, in around end of 2019, Exor (owned by the Agnelli family) bought into CLVT as a long term investor with a board seat.

So it’s 2020 and CLVT is partially owned by Exor with its previous owners BPEA and Onex (both were selling down).

All in all, Onex and BPEA still had a meaningful stake of roughly ~26% and Exor had a small minority (as part of the secondary sales from Onex and BPEA). The rest were other public insitutions.

It doesn’t stop there. Now that all the new shareholders are in place in 2019, we move on to 2020. By this stage CLVT spotted a new acquisition target that management believed would add value to the business. This was CPA Global.

Originally, CLVT focused on upstream IP activities such as research, prior-art analysis, and patentability intelligence, but it did not directly handle filing or administrative execution. CPA Global, on the other hand, specialized in downstream IP administration, including portfolio management, renewals, and workflow support. The acquisition was intended to increase customer stickiness by embedding CLVT more deeply into day-to-day administrative processes.

So CLVT decided to buy CPA Global for an enterprise value of ~$6.8 billion. Here is the interesting part: as part of the deal, the CPA Global owners, which included Leonard Green and Partners Group (two shrewd investors) would retain roughly 35% of the combined entity post-close. So this was a non-cash transaction. At this time, CLVT assumed the debt of CPA Global, which made the combined entity highly leveraged.

Side note:

So when you see a deal like this, where the acquiree accepts shares in the combined entity instead of cash, it can mean many things and this is where judgment comes to play. My belief is that Leonard Green and Partners Group saw huge potential after this acquisition, and were willing to retain ownership to ride the growth of this new company. Otherwise they would have asked for cash when they sold the company. Instead they kept shares…

And it doesn’t stop there…

CLVT decided to acquire another company in 2021 called Pro Quest with debt + equity. The owners of Pro Quest accepted some cash (which CLVT used from tapping debt) and some equity. Unlike the previous owners.

Now based on my limited research, it turns out that the company was not materially impacted by covid due to the sticky nature of its business, although new accounts slowed, but overall it did not impact the business (a good sign). That said, the growth of the business and integration did not happen as planned, and the valuation during the acquisition in 2020 assumed that there would be growth.

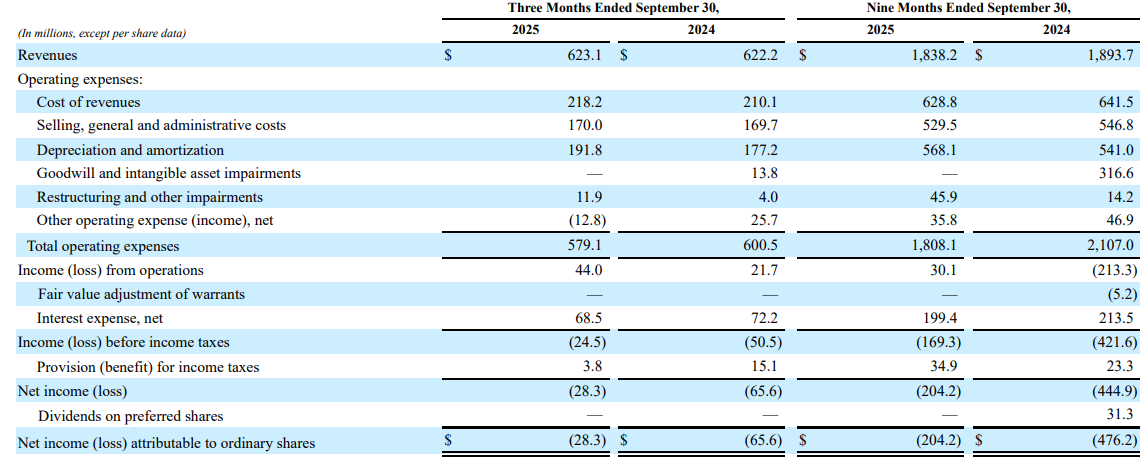

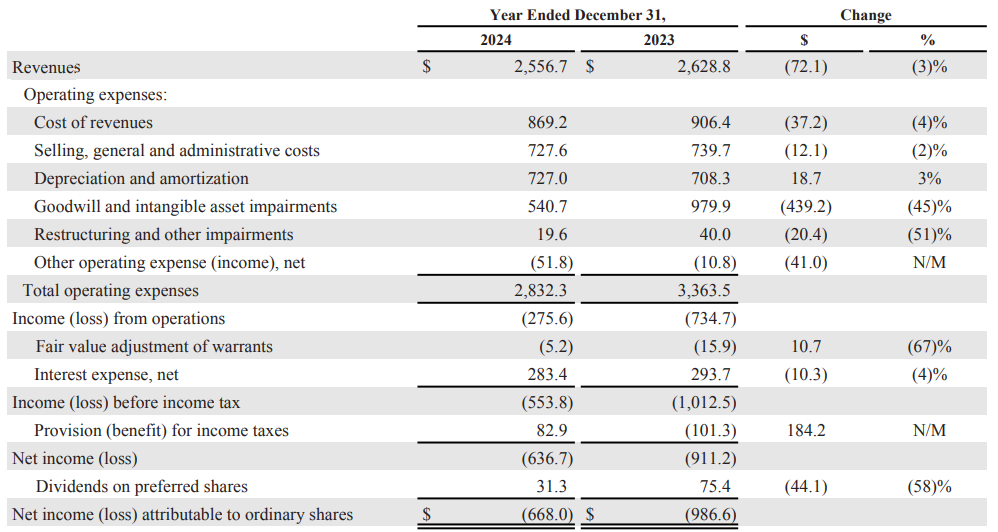

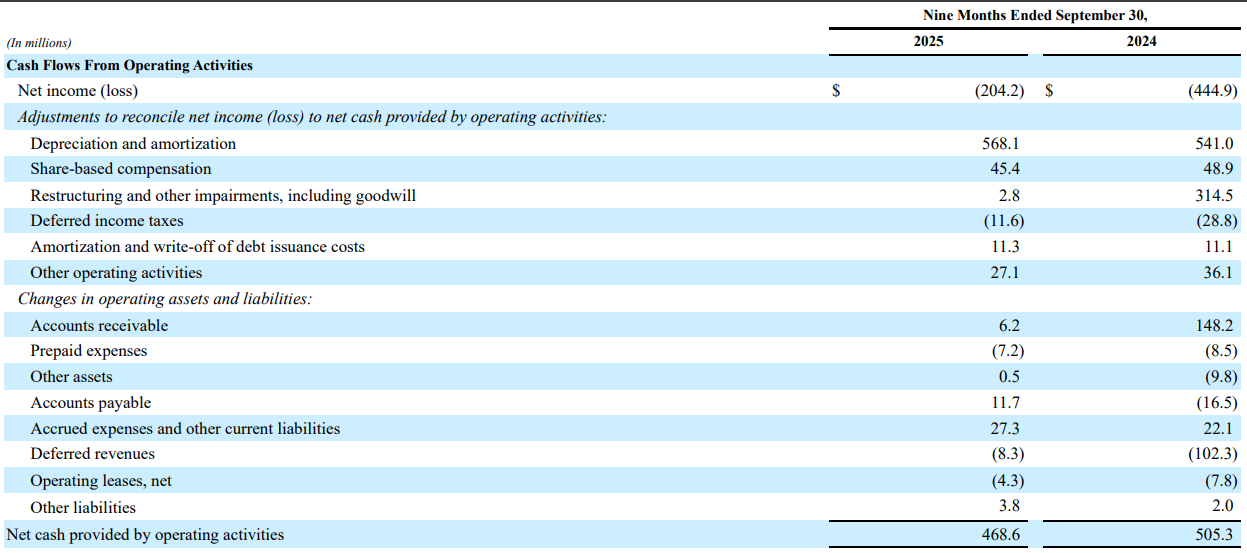

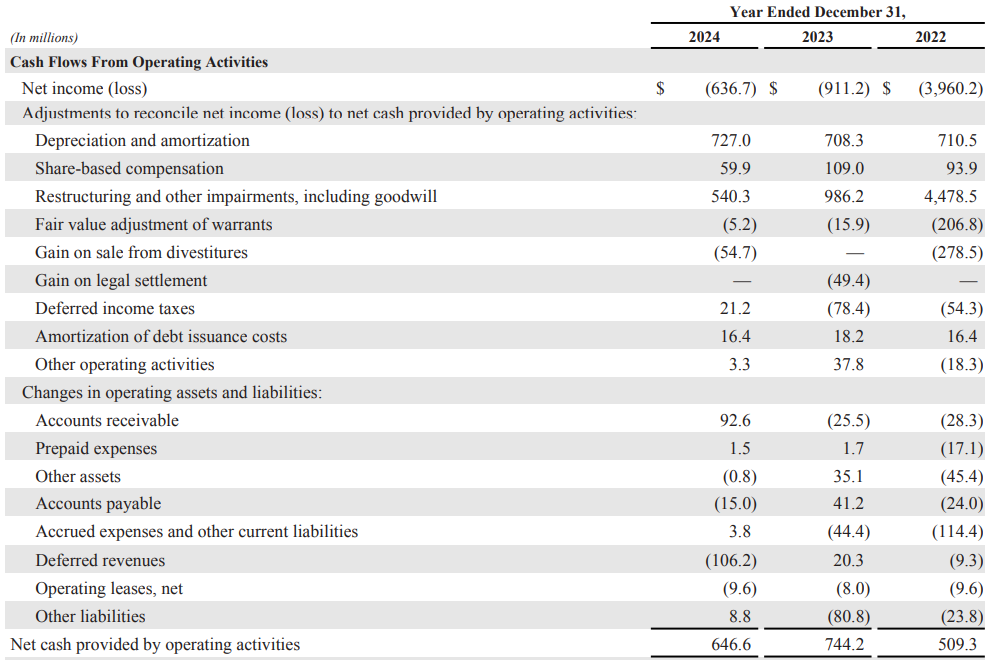

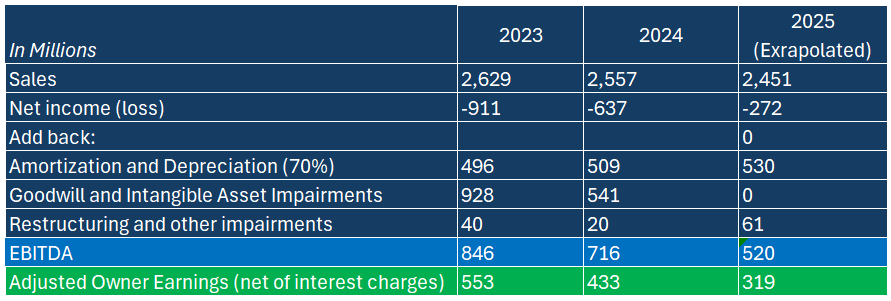

Now the company was left with high debt and significant impairment charges, which impacted earnings, as shown below:

10Qs

10K

There are a few things worth noting here:

Depreciation and amortization were mainly from acquired intangibles from their previous acquisitions. CLVT has hardly any hard fixed assets being in the software business. It is fair to say a chunk of these came from the acquired trademarks of the aquiree companies. It is probably justified to add 70% back, and let’s just assume the remaining 30% come from computer hardware and parts.

According to their audit report (from PWC), management had to admit the Life Sciences & Healthcare unit was worth less than previously assumed. Result: Two goodwill impairments were recorded in 2024: (1) ~$303M mid-year and ~$149M at year-end. This makes up the majority of the $540M impairment charge. These are non-recurring and non cash. These are also penalties for past mistakes, and not prospective in nature and has nothing related to how the company is run. It says one thing: they made a big mistake acquiring those companies.

Restructuring and other impairments came from related costs to previous acquisitions, which is non-recurring and non operational in nature.

This business earns a high return on invested capital as it doesn’t require significant capex for incremental returns.

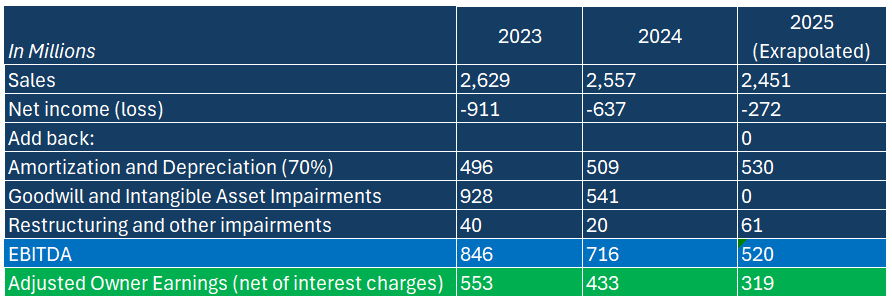

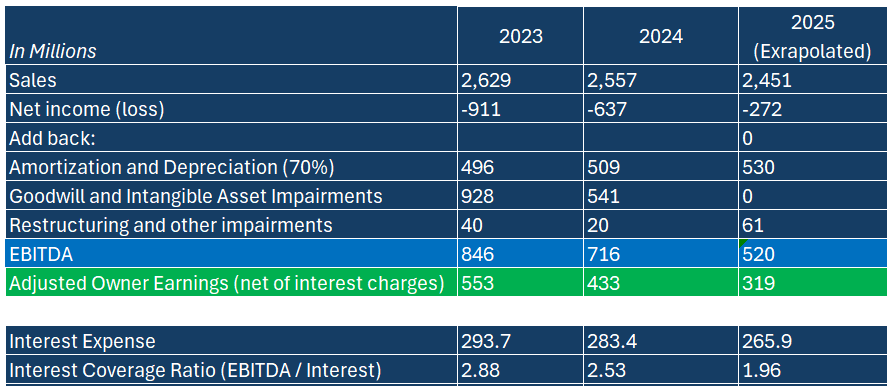

All in all, the adjusted earnings would look something like this:

What this tells me is that after adjustments, CLV still produces meaningful owner earnings, but those earnings are declining over time, confirming a pressured, non-growing business whose equity value depends on balance-sheet relief rather than improving fundamentals. If you look at interest expense, they make up a good a good chunk of expenses.

Now to the cash flow statement:

The company spits out cash despite it’s high debt burden. One thing to note is that deferred revenue is an important line item here. Being a subscription business means that it cannot declare revenues when the money is paid by customers. This is because the service has not been rendered. So in this kind of business, you can argue that deferred revenue should be added back to revenues. But I will not do this since earnings is a performance measure, not a cash flow measure. For the sake of operating cash flows, we need to add it back.

What is more telling is the trend: 2024 was a year of restructuring and customer tightening, reflected in a big drawdown of deferred revenue. it could be that contract expansion stalled. In 2025, deferred revenue stabilized, indicating that while customers are no longer expanding, they are continuing to renew. This suggests Clarivate has high cash flow quality but lacks growth.

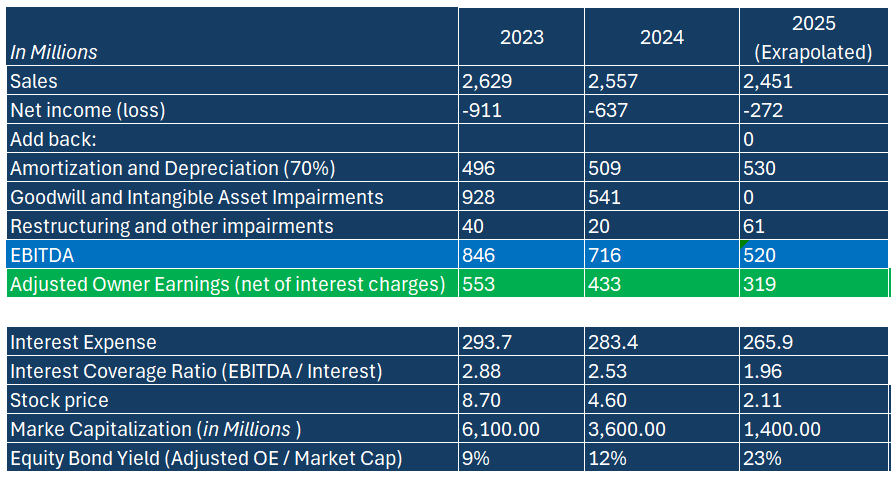

There is something that is telling here: CLVT still generates cash flows despite its high debt burden, and is able to meet those interest obligations with the interest coverage ratios shown below:

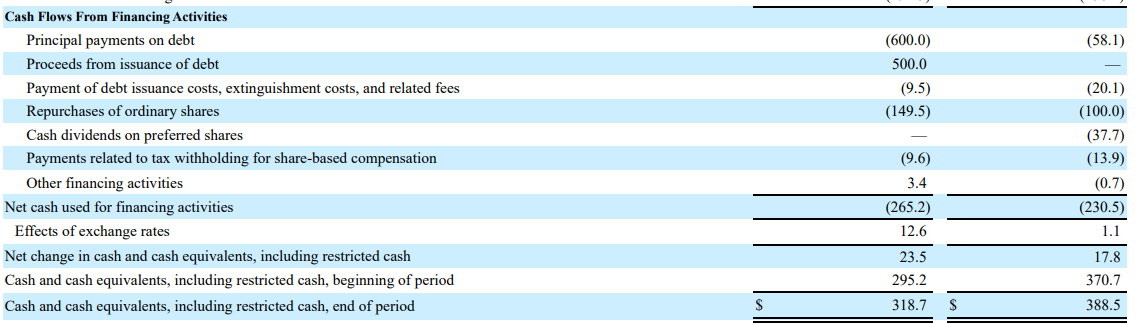

On top of this, it seems that they have been pairing down debt and at the same time management has been buying back their own shares.

In 2025 it shows that they refinanced some of their debt ($500M) and paid down $600M. This is a net reduction of $100M and it’s associated financing charges (a good sign).

Two days ago, they decided to redeem $100M of their senior notes as announced here.

It also shows that the company bought back $100M and $149.5M worth of shares in 2024 and 2025 respectively. A sign that they are confident in reinvesting in their own company.

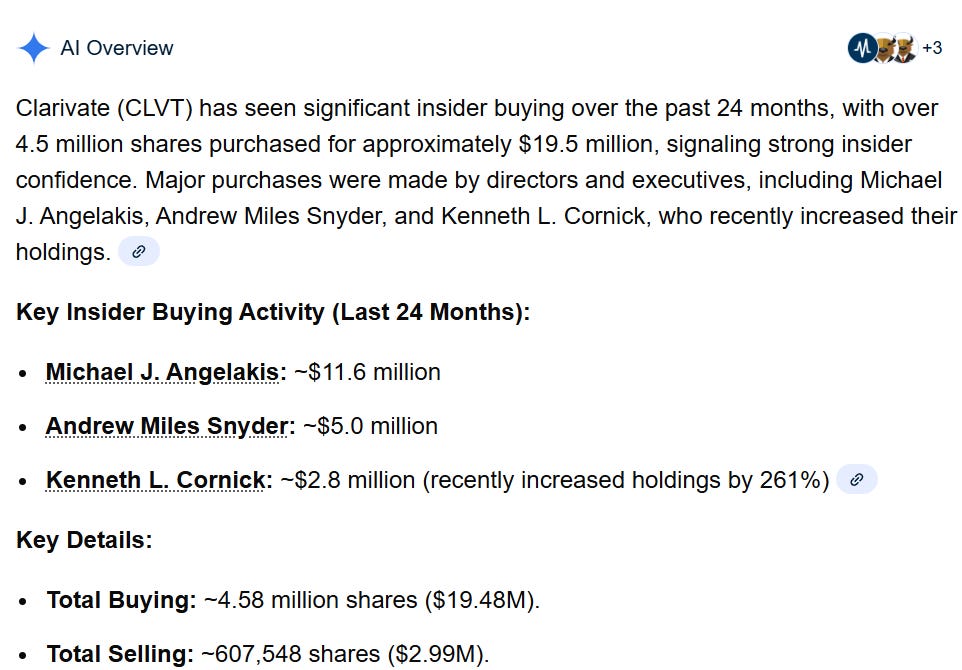

On top of that, insiders are buying:

These are all signs that they might have an edge. They may see value that the market doesn’t. It is also interesting that insiders own 23% of shares outstanding.

So by now, we know:

Clarivate generates enough cash flow to meet debt payments.

Owner earnings deviates significantly from accounting earnings (in a good way).

Insiders are buying and continue to buy.

The company has been pairing down debt.

The company balances debt repayment with share buybacks, potentially seeing value in their own shares.

The question is: given the level of owner earnings, what should be its intrinsic value?

I am a yield investor and like focusing on companies with sticky sales and earning power. Let’s revisit their sales and earnings:

What this shows is that Clarivate is a slow growth (or even slightly negative growth) company with positive cash flows and a highly leveraged balance sheet. Despite that, there is value based on the non-accounting earnings shown above.

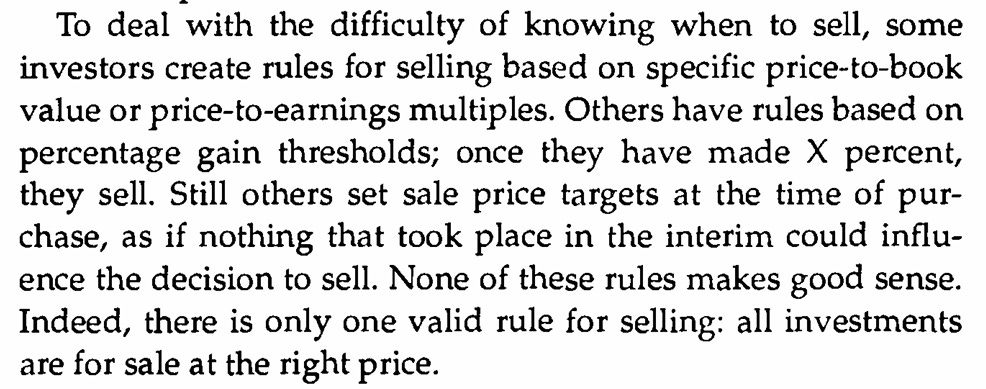

One of the things I learned from Joel Greenblatt and Seth Klarman is their focus on Margin of Safety. Joel Greenblatt likes to say “Look down, not up.” and Klarman said the following from his book:

In this case, I’d like to focus on value and price today, and we can explore when to sell based on what kind of price is considered “right”.

There is a method I like called the Equity Bond Yield. The Equity Bond method is a way to value companies with stable and recurring earnings. It helps investors understand how much they earn in the form of yield, which they can then compare to other investments. The idea is to treat owner earnings like the coupon on a bond. Instead of dividing the coupon by the bond price, you divide owner earnings by the company’s market value. This gives an equity yield that shows how much cash the business produces for owners at today’s price. Warren Buffett has said that stocks can be viewed as bonds with changing coupons. This method helps investors judge whether the earnings yield is attractive for the risks associated with this opportunity.

So what is the Equity Bond Yield of Clarivate using owner earnings?

Keep in mind, that current owner earnings assumes high debt (it incorporates interest charges), so you can imagine how much this yield can expand if debt is paired down. Management has been making an effort to pair down debt (as shown earlier) and with efforts to buyback stock. Given the yield, it is enough for me to say that I don’t need to do the math on how much this yield can expand, as I know that there is a margin of safety in this implied yield. You protect your downside, the upside takes care of itself.

It seems that with an equity bond yield of 23%, they will have to play the balancing act of improving the balance sheet (pairing down debt) and capturing value (buying back shares) at the same time. This may explain the reason behind their financing activities in their cash flow statement.

To be conservative, I would place the fair equity bond yield for this company given its broken balance sheet at say 12% (this is my personal required yield). Even if we assume 12% as being fair, owner earnings would have to drop to $170M from its current $319M, which I find drastic.

Think of this as the level of earnings where you would consider selling (as a worst case). If this were to happen, the company would have to lose 25% per year in owner earnings to hit roughly $170M by end-of 2027.

This does not assume that the company pairs down debt. If they do, then it is all upside.

So at today’s price ($2.11) I find Clarivate to be undervalued, and if 12% is the ideal equity bond yield for this kind of company (assuming double digit for a slightly damaged balance sheet), and assuming management pairs down debt, this gives an implied intrinsic value of between $1.87 (worst case) and ~$3.50 (realistic best case with upside for more depending on how they fix their balance sheet) when you start using a data table assuming different owner earnings and yield:

The biggest risk I find with this company is if management does a poor job allocating capital. For example if they decide to pursue more acquisitions that don’t add value, or if they are too aggressive on buybacks at the expense of maintaining a poor balance sheet. The big assumption I have is that management is good enough (based on the last 3 years) to allocate capital to capture trapped value, which I believe the market is not seeing. This is a perfect example of when a company’s true fundamentals are hidden by accounting earnings. But time will tell whether certain things play out.

Now, there are many things that I might be missing, but as Keynes once said, it is better to be roughly right than precisely wrong. In this case, I am willing to pull the trigger given the risk/reward situation of this company.

As an investor, the equity bond framework helps assess which yield is reasonable given a level of owner earnings that is adjusted for economic reality. Intrinsic value is personal and depends on one’s required rate of return. My return threshold, given the risks of this business, may differ from that of other investors. That said, at today’s price, I believe Clarivate is undervalued, with upside that depends on the earnings and yield assumptions outlined in the table above.

In my view, $3.50 per share represents a conservative long-term estimate, assuming the following conditions hold:

Sales remain broadly stable, with modest fluctuations in owner earnings. This is not a growth investment.

Management continues to reduce debt prudently in the next few years.

The company avoids further acquisitions unless they are clearly opportunistic and highly attractive.

If some of these don’t play out with hiccups along the way, it may fall to a lower intrinsic value. So at any moment in time in the future, we can assess whether the price is considered “right”.

Clarivate is in the middle of a turnaround to fix its balance sheet, and even under a conservative case, the equity appears undervalued. I would approach this with a minimum three- to five-year holding period, and to consider the fact that there may be unforeseen risks along that way that would warrant selling this position. The company’s next earnings call is scheduled for February 24, which should give further insight into their future capital allocation plans and sales momentum. Until then, Clarivate deserves a small position within the portfolio.