Beyond Exits and Dividends

Aligning entrepreneurs and investors towards long term value

When entrepreneurs embark on a journey of raising capital, they encounter different types of investors. These investors vary in terms of knowledge, time horizon, risk tolerance, and financial objectives. Amidst this diversity in views and risk tolerance, there are several questions that shed light on the nature of investors and whether entrepreneurs should consider accepting funding from them. Raising capital for your business is not merely about securing any available capital; it's about securing the right kind of capital.

One of the frequently posed questions by prospective investors is, 'What is your exit strategy?' or 'When can I expect dividends?' While these questions may seem reasonable, they don’t align with early-stage companies, and here's why:

Exits

An exit, in essence, is the natural outcome of a company's growth and development. It is the result of building a business for the long term. Companies that are committed to long-term success tend to achieve exits naturally as they pursue their long-term objectives. The notion that an entrepreneur should build a company with the primary goal of exiting can potentially divert their attention towards short-term objectives aimed at appeasing investors seeking quick returns, which can, in turn, diminish performance.

Consider some of the biggest and most successful companies today, such as Amazon, Facebook, and Berkshire Hathaway. Their success has been grounded in long-term vision and the establishment of sustainable businesses. Mark Zuckerberg, for instance, turned down a $1 billion offer from Yahoo in 2006, a decision many viewed as unconventional at the time. As of this writing (~18 years later), Facebook’s market capitalization stands at $772 billion, or 772x Yahoo’s offer in 2006. Jeff Bezos’ first angel round was $1M for 20% of the business. You can only imagine the fortunes those early investors made by sticking around (Amazon today still does not issue dividends). Some might say “well that is Amazon and Facebook, they are different and we will never be like that.” Well, the effects of compounding work the same way regardless of what business you have, so long as you are growing and are profitable. The key takeaway here is that an entrepreneur's primary objective should be to build a robust and enduring business for the long run, rather than treating their company as a mere financial instrument to be quickly sold or flipped.

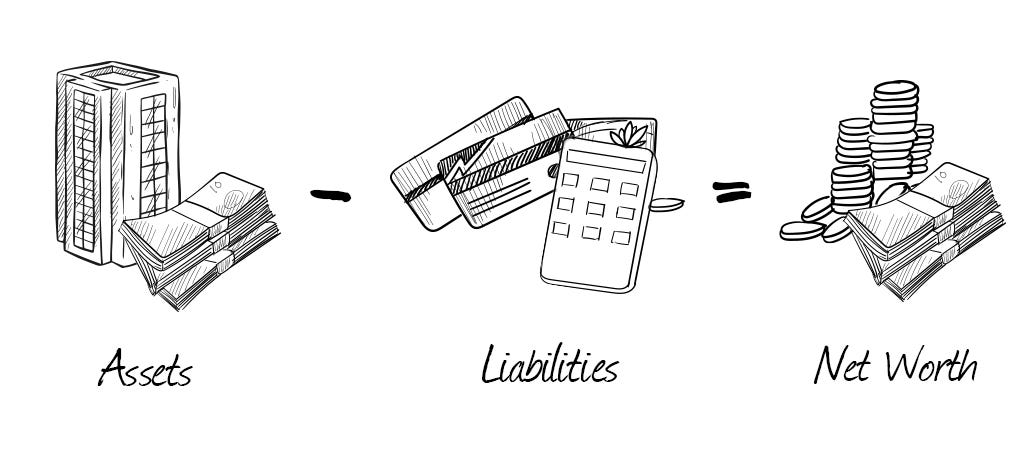

For investors, the crucial consideration should not solely revolve around the amount of cash generated tomorrow, but rather on the overall increase in wealth over the long run. Wealth is not solely determined by cash holdings; it is determined by overall assets owned (A) relative to liabilities incurred (L).

Assets represent the value of the company's properties and should be reflected in the equity held by investors. Liabilities are any personal debt an investor may have. When an investor's assets exceed their liabilities (A > L), they hold a positive net worth; conversely, if their debt is greater than their assets (L>A), they have a negative net worth. In essence, wealth is about growing one's net worth, and investments in companies provide an avenue for potential wealth accumulation.

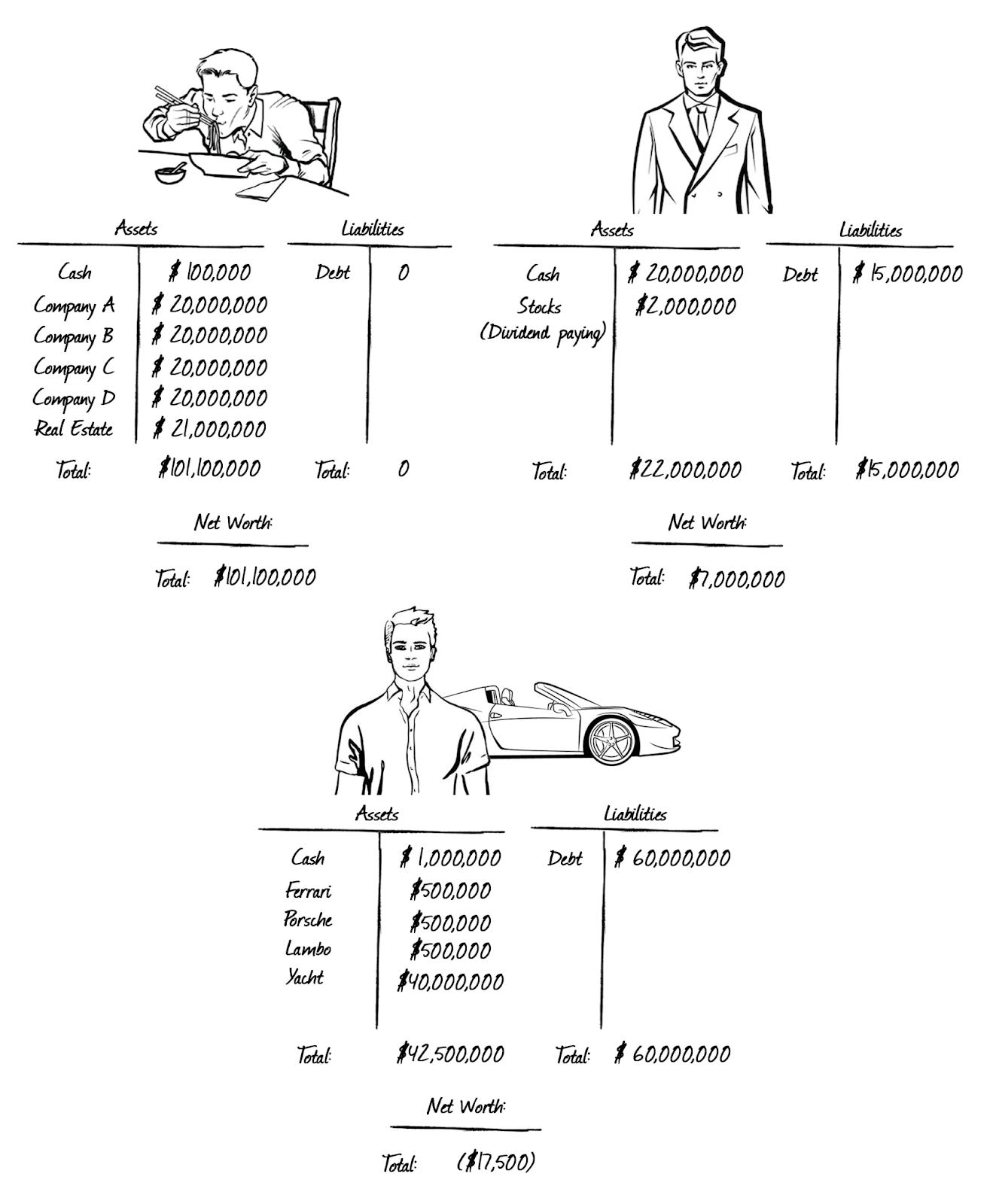

Above, you see three types of people: the instant-ramen-eating-entrepreneur/investor, the guy with a suit, and the guy with a Ferrari. At first glance, the average person would probably point out to the guy with a Ferrari or suit to be the wealthiest of all. The reason for this is that society places a premium on materialism, and as a result associates wealth with it, but this is usually not the case. This might be an extreme example but extreme cases are meant to bring the point across (although the above is grounded in reality), and understand why some entrepreneurs live frugally despite huge funding rounds. This is also the reason why most self-made billionaires are frugal. It’s not because they are hoarders or misers, but because they understand the true value of money (as a means to wealth). If they are self-made and have gone through the natural cycle of building a company, then they will understand how valuable each dollar is to them. This is also why we at DayOne place frugality as being one of the highest virtues for entrepreneurs.

Therefore, the kind of investor an entrepreneur seeks should understand this concept and recognize that their investment is intended for long-term growth. This entails leaving cash within the company, with the understanding that it will be deployed into ongoing operations or used to acquire other assets, contributing to the company's growth and profitability. Most, if not all, individuals on the Forbes list today have attained their positions primarily through equity ownership.

Dividends

The issuance of dividends is dependent on the amount of surplus cash available for distribution, and only if there is a lack of compelling growth opportunities within the company. There are two approaches: The residual approach and the stability approach.

The residual approach argues that companies can use internally generated funds for dividends if all project capital requirements are met, and only if there is excess cash after all projects are met will it be allowed to distribute dividends to shareholders.

The stability approach, on the other hand, is when a company sets a policy of a fixed payout based on how much it earns per year. In the case of early-stage companies, they require every cent to reinvest in their current operations, making the topic of dividends a non-starter. The stability approach doesn’t apply either since most early stage companies are unprofitable until their growth rate subsides.

But is there ever a point at which a company can afford to give back to investors? Sure, as retained earnings grow and capital project funding is met, this option emerges. That said, having excess cash within the company is never a bad thing. Excess cash can fuel acquisitions, expansion or serve as a rainy-day fund for unforeseen corporate events, allowing companies to be nimble enough for unique opportunities that arise.

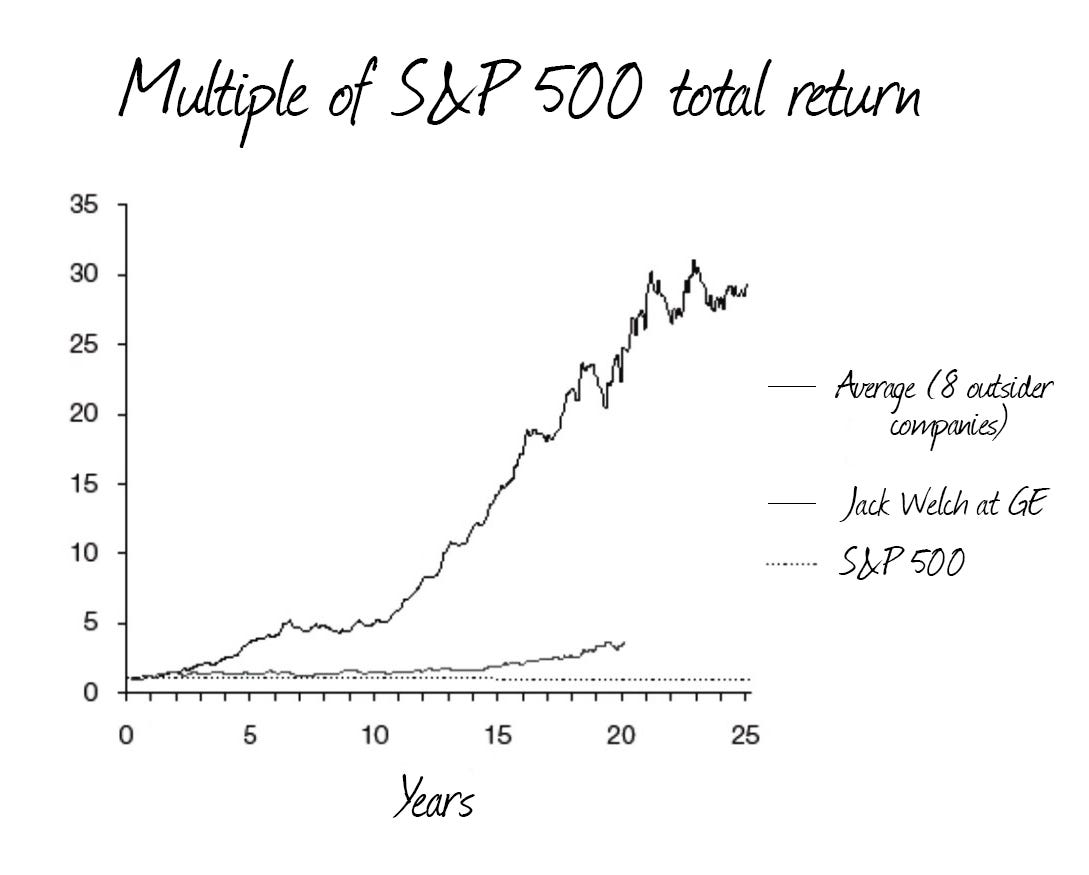

As a company grows, its financial position is regularly evaluated, and decisions are made regarding the utilization of cash. This responsibility typically falls on the capital allocator within the company, often the CEO or CFO. A great resource on this topic is William Thorndike's book, 'Outsiders: Eight Unconventional CEOs and Their Radical Footprint for Success.' Thorndike chronicles the methods employed by companies that outperformed the S&P 500 by over 20 times over a 25-year period. One commonality among these companies is their avoidance of dividends in favor of utilizing internal cash. What he found is that all shied away from dividends and prioritized the recycling of cash for future growth, and it’s no surprise that every single one of them was frugal.

When a company performs well, it generates significant free cash flow, providing various options at the end of the fiscal year, including:

1. Investing in existing operations.

2. Acquiring other businesses, either vertically or horizontally.

3. Reducing debt.

4. Repurchasing company stock.

5. Issuing dividends.

The top-performing companies have proved that following the first and second approaches above yields the most favorable results in terms of company value. They utilized excess free cash to drive operational expansion, either by reinvesting in current operations or pursuing value accretive mergers and acquisition (M&A) opportunities (many also repurchased their own stock). It’s almost as if they established an in-house M&A task force dedicated to consistently identifying attractive long-term opportunities, and they maintained a strong commitment to this approach.

In the case of a rapidly growing company, dividends should not even be on the radar. Dividends, when declared prematurely, can be seen as a form of wealth leakage. For every dollar taken out in dividends, there is an opportunity cost in terms of the dollar's potential growth rate within the company.

It's crucial to bear in mind that wealth isn't generated through cash payouts; rather, it's built through the ownership of appreciating assets over time. If an investor's primary motive is liquidity, with the intent of converting assets into cash, that is a very different motive, and it’s important for entrepreneurs to understand this at the outset. Early-stage companies require time to mature and achieve their full potential. This necessitates a degree of patience from investors, and it is often this patience that paves the way for substantial returns in terms of net worth.

“Someone’s sitting in the shade today because someone planted a tree a long time ago”

- Warren Buffett

One way to look at this is to consider cash as a means to wealth. It is a token that allows you to build wealth and should not be considered an end state in-and-of-itself. Cash, real properties, and companies are all interchangeable — they are all assets. Owning each type of these assets should give you the same level of satisfaction as it relates to wealth. Unfortunately, we live in a society where materialism prevails, and the only way to have access to a life of materialism is through cash (you cannot convert a portion of your real estate or equity to a Louis Vuitton bag). What’s more important is to seek liquidity that gives you enough freedom to live your life and use any excess cash for wealth building, and these are the types of investors you should find. Those who are already independently free, and have a deep desire to build long term wealth.

For investors, the question shouldn't center on "What's your exit plan?" or "When will I receive dividends?" Instead, a better question would be: "What's your end goal?" As an entrepreneur, I believe the most compelling response is straightforward: "To maximize shareholder wealth."

ABOUT THE AUTHOR

Keenan Ugarte is Managing Partner at DayOne Capital Ventures, an independent private holding company based in the Philippines that partners with entrepreneurs across a wide range of industries. He is the Co-Founder and Director of The Independent Investor.